Whichever way Brexit vote turns out, it’s a ‘no win’

for Europe

Britain’s EU referendum is the big risk event global markets are dreading. It could be a nightmare scenario, threatening to trigger a chain reaction that could plunge markets back into a new global catastrophe. The real worry is that the world is already slipping back into a black hole of uncertainty whichever way the vote goes. This time there may be no easy way back.

No wonder world policymakers

are panicked. While European Council President Donald Tusk clearly over-exaggerated

by warning Brexit could mean the end of Western civilisation, both the IMF and

OECD are deeply alarmed about the consequences for the world economy and

financial markets. The major central banks are already drawing up contingency

plans and getting ready to intervene if the UK votes to leave the EU and

markets descend into chaos. It is hard to see what they can do. Global

currency, credit and equity markets are already highly agitated.

Europe should be especially

worried. Whatever happens in the Brexit vote, Europe will feel deep shockwaves.

It is a 'no win situation', with Europe standing to lose whichever way the vote

goes. Europe is not long out of the 2009-2013 euro zone crisis and it has taken

huge stabilisation efforts from EU governments and the European Central Bank to

stop European monetary union and the euro falling apart. It would not take much

to open up old wounds and set Europe lurching off into new economic and

financial disorder.

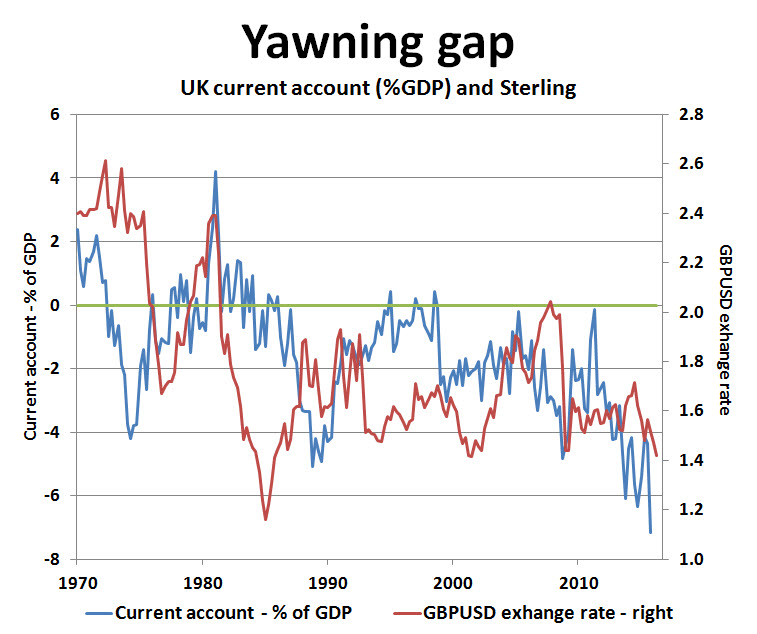

A 'leave' vote will have an

immediate impact. Capital flight out of the UK, a sterling currency crisis and

the threat of economic ruination would hit British markets especially hard.

Europe would not be spared and market speculators would quickly home in on

contagion risks spilling over into the euro zone. Economic and financial

stability would be knocked off its perch. The bears would scent blood and begin

the hunt for 'who goes next'.

Even if the UK votes to

'remain', the barn door has been opened far too wide on European disintegration

risks. Despite all the healing balm thrown into the ring from the ECB's

monetary super-stimulus in the last seven years, the same old problems persist.

Europe remains deeply divided, split between the economic haves and have-nots.

Extremely rich and powerful Germany juxtaposes on the one side with struggling

euro zone nations like Greece, Portugal and Spain on the other.

Immersed in deep debt,

stifled by austerity and dogged by rampantly high unemployment, there is little

chance of long-lasting economic recovery for these nations, especially

considering the extremely challenging global backdrop right now. The threat of

hard landing in China, instability in emerging economies and now the threat of

Brexit contagion all pose serious dangers ahead for struggling euro zone

nations. But there are bigger elephants in the room, not least growing

anti-austerity protests in France and the risk that Italy falls victim to the

deepening investor gloom.

If the risk of Greece going

into national insolvency threatened to up-end global markets, the threat of

Italy going into a banking and government debt default would be nemesis for the

world economy. The problem would be far too great for the ECB’s limited

resources to cope with. The recent election successes of the populist anti-austerity

Five Star Movement underlines that there is a ticking time-bomb under

conventional Italian politics. Italy remains the sleeping giant of the euro

zones’ Doomsday disorders. In time Italy will come back to haunt the markets.

Despite the drive to negative

interest rates, the glut of QE money and the high official ramparts surrounding

the euro zone's vulnerable financial markets, the ECB's monetary defences are

far from impregnable. With market jitters becoming more acute, peripheral yield

spreads are already widening relative to German government bonds on safe haven

flows. If markets decide to take on the ECB, it could trigger a dangerous

re-run of the 1992-1995 and 2011-2012 deconvergence bloodbaths. European

markets are highly vulnerable.

The real worry is that EU

policymakers continue to kick the can down the road without solving the real

economic and social inequalities dogging Europe. As long as Germany gets

stronger, at the expense of the weaker European nations, political divisions

will widen and the cohesive forces holding Europe together will continue to

fragment. Anti-austerity protests and political extremism are on the rise and

leading to deepening antipathy towards Brussels and the EU.

These trends are crystal clear in

the usual suspects like Greece, where up to three quarters of voters are

dissatisfied with the EU. More alarmingly similar trends are showing up in core

countries like Austria, Netherlands and France which are witnessing the

emergence of more inward-looking, nationalistic and anti-EU tendencies. It

bodes badly for the future.

There is much more at stake

in Britain's Brexit vote. The survival of European unity, the single market and

the euro is on the line. Investors have good cause to be alarmed.

So far, the euro seems to be holding steady by default. Once the Brexit vote is out of the way, the markets will inevitably return to the thorny issue of Europe’s deepening political fractures and place their bets on eventual euro break-up risks down the line.

Euro parity versus the US dollar still beckons. Europe is not out of the woods by any stretch of the imagination, with or without Britain.