It is no exaggeration to say that

Britain stands at the edge of disaster. In two weeks time, UK voters will be

making a momentous decision that will shape Britain’s future for generations.

As the nation heads to June polls on whether to remain in or leave the European

Union the stakes are high. A majority vote

in favour of a British EU exit (Brexit) could lurch the country into chaos for

years. Its impact will be felt around the globe.

Britain is heading into the

unknown and the country seems worryingly split down the middle. Judging by recent

surveys, public opinion seems to be edging towards the Leave camp. If this continues,

the final run-in to the referendum will be an anxious time for the nation and a

source of rising instability for Britain’s financial markets.

International confidence in

the UK could be shaken to the core. Britain’s strong growth record, its leading

role as a global financial centre and even the survival of the 300-year old

British union will be under a cloud. If Britain crashes out of Europe, Scotland

has threatened another independence vote in order to stay inside the EU.

Britain’s influence as a leading international power would begin to wane.

The main credit ratings

agencies have already warned they would take a dim view of UK assets on a

British break from Europe, warning that a sovereign downgrade might be inevitable.

International confidence in UK investments would suffer badly. Britain is no

stranger to currency crisis and the pound could take a beating. International

investors would shun stocks, government bonds and industrial assets in the

uncertainty. And it might take years before the UK can strike a favourable EU

trade deal and forge a new working relationship with Europe.

International investors could

lose out heavily, especially those that were coaxed into investing into Britain

under Margaret Thatcher’s private sector renaissance in the early 1980’s, when

international companies began flooding into the UK. Under sweeping structural

reforms, Britain became a Promised Land of free enterprise and market-friendly

deregulation for foreign investors. The added advantage was free admission into

Europe’s single-market, with front-door access to the EU’s 500 million-strong consumer

market.

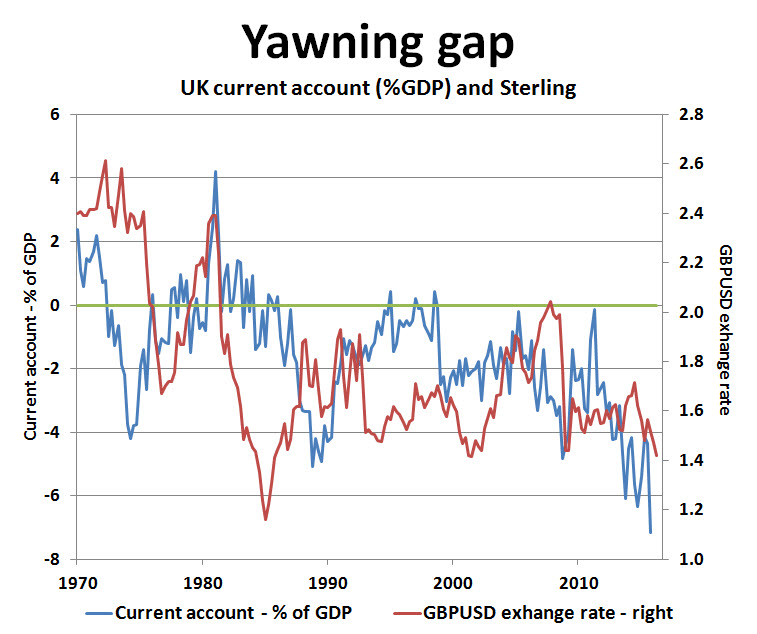

Over the years, this has

reaped rich rewards for Britain and brought strong inflows of foreign direct investments

(FDI). Inward FDI has helped finance the UK’s current account deficit and

provided vital support for the UK’s asset markets. The UK now stands as the

world’s third largest destination for inward FDI behind the US and China, with the

stock of FDI investments in Britain currently around 1.7 trillion US dollars.

The UK is the top target for FDI flows into Europe thanks to Britain’s track

record on providing a safe port for foreign money. All this could change very

dramatically.

A beneficiary has been the UK

car industry where Asian companies are major stakeholders. Since the 1980s, Japan’s

Nissan, Toyota and Honda have built up significant UK manufacturing presences,

while India’s Tata Motors has owned Britain’s Jaguar Land Rover since 2008. Any

threat to Britain’s free trade access into Europe would cast these investments

into doubt. Any barriers to free trading would be bad news for UK-based

manufacturers and momentum to quit Britain and switch production to Europe

could turn into a stampede.

As the United States learnt

to its cost under the strong dollar regime during the mid-1980s, when many US companies

switched manufacturing overseas to stay competitive, it has been extremely hard

to win back business that has moved offshore. The US’s yawing trade gap is

testament to that. Britain could end up in the same boat if international

companies panic about losing eligibility for free trade status in Europe. FDI inflows

would reverse, tearing a large hole out of Britain’s industrial capacity in the

process. It would be bad news for UK growth prospects, for the balance of

payments and for British industrial prestige.

Indeed, there is a possibility

that Tata Steel’s recent decision to quit UK steelmaking is less to do with

global over-supply and heavy loss-making in their UK plants and more to do with

a loss of confidence in Britain’s industrial future due to Brexit fears. In

addition, recent news of Tata Motors plans to build a factory in Slovakia, its

first European JLR car plant outside the UK, could be a bad omen for British

car manufacturing shifting into Europe if Brexit takes off.

Brexit also poses serious

risks to Britain’s future as a global financial centre. The UK financial

services sector is a vital part of the economy, employing over one million

people, accounting for 12 per cent of total output and 11.5 per cent of UK

government revenues. The City of London is not only home to over 250 foreign banks,

but also the European headquarters for many of them. If Britons vote to leave

the EU, London faces losing one of its top money spinners – the multi-trillion

euros traded-derivatives business which the ECB would like to see housed on

European and not UK soil. Furthermore, many foreign banks based in the UK might

find it more prudent to comply with the EU’s regulatory framework by moving to

Frankfurt or Paris. Brexit could spark a major bank drain out of Britain.

Britain’s economy looks

vulnerable. Since the global financial crisis, the UK has grown faster than its

Group of Seven partners, but only thanks to the economic fizz of zero interest

rates, quantitative easing and loose fiscal policy. Without these policy

boosts, underlying UK growth potential would be nearer to 1.5 per cent than the

latest 2.0 per cent headline rate. The shock of Brexit, a quick foreign exodus

out of UK investments and a collapse in British productive capacity and jobs

could hit confidence hard, tipping the economy into a nasty recession.

In the worst case scenario,

the UK could fall into a deep depression. Unfortunately, UK policymakers are

running out of options to deal with new crises. UK interest rates are already

at rock bottom and QE has already run its course. A sharply weaker pound would

only be a small fillip for what little would remain of UK manufacturing locked

outside of Fortress Europe. Foreign investors would be hit hard by the fall in

their sterling-based assets. For international manufacturers, banks and

financial services companies there are compelling reasons to get out quick

while the going is good.

No comments:

Post a Comment