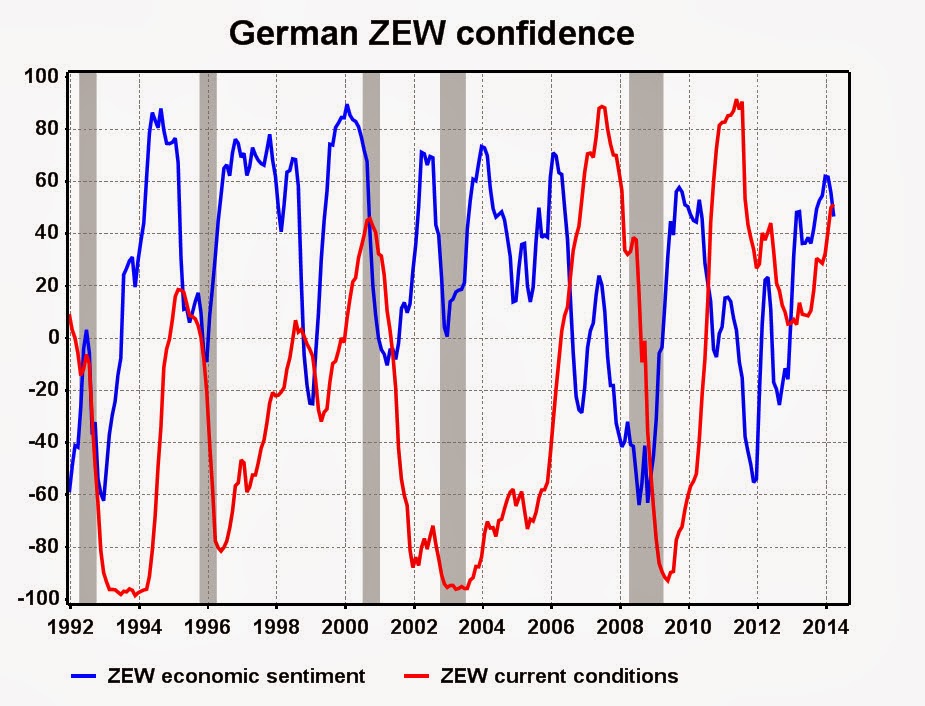

The Eurozone CPI data signals an imminent ECB rate cut. March inflation dropped to 0.5% from 0.7%. Eurozone inflation is sliding inexorably towards deflation. The ECB is duty

bound to ease monetary policy very quickly. This week’s ECB policy meeting

should be a catharsis. The options are clear. The recovery is struggling.

Unemployment is close to a record high. And deflation risks are pressing. It is

High Noon for a radical policy move this week. The ECB can move interest rates

into negative territory. It can give the green light to real quantitative

easing. The ECB can build up the whispering campaign for a weaker euro. It can

enact one at a time, or it can be radical and do them all together. Clearly,

the ECB has nothing to lose. Traditional opposition from Germany’s Bundesbank

already seems to have melted away. Bundesbank Chief Weidmann has already given

tacit support for all three policy initiatives. The way ahead is clear. The ECB

simply has to seize the moment and set the Eurozone on course for a

sustainable, job-creating recovery ahead. The key casualty will be the euro.

Right now it is standing on a trapdoor. It will fall very far and fast. At

return towards fair value around USD1.20 looks a safe bet in the coming months.